Double entry accounting refers a system where transactions for a company are recorded both in debits as well as credits. Both the accounting equation approach, as well as the traditional, use two aspects in transactions. The real account debits are what is sent and the personal accounts credits are what is received. As with credit and debit, both are recorded in different books. These are some of the fundamental concepts behind double entry accounting. Hopefully, you'll understand its basic concepts.

Credits and debits

Double entry accounting for credit and debits has two major categories: the debit and the credits. Using this system, debits are posted to the left column of an account and credits are posted to the right column. The credit is always greater than the debit. Credits are generally more expensive than debits. The amount of credit equals the debit. The account balance equals the sum of the debit/credit.

Daybooks

Daybooks are important documents in a double-entry accounting system. Each transaction is kept in at least two ledgers. A debit is charged to the customer's ledger account and a credit to that account. The daybooks can be used to assist businesses in keeping track of their finances. However, daybooks are not a substitute for a nominal ledger. Before making the switch from single entry to double entry, you should carefully consider your business's needs and goals.

Nominal ledger

When a business conducts transactions, they are recorded under the name of an account and the date of the transaction. You may have different types of journals. A special journal for cash transactions is one example. These journals document specific transactions and are typically omitted in the general journal. These journals are then combined into the nominal journal. This document lists all transactions that took place during the period. It serves as the basis for financial statements about cash flow.

Balance sheet

A double-entry balance sheet includes three components: assets and liabilities. Equity is the third component. Assets are the items owned by a business, such as cash, machinery, and buildings. Liabilities refer to what the business owes others. Equity represents the owners' stake in the business, such as their contributions or their share of the profits. This accounting system is essential for understanding how each element affects the others.

The most widely accepted accounting principles

Financial accounting is based on the principle of double-entry. This principle ensures that assets as well as liabilities are equal and that their total is always in balance. Double-entry accounting, which is popular among investors and banks, is a standard practice. Double-entry accounting is flexible and allows for custom adjustments. The principles of double-entry bookskeeping are as follows.

FAQ

What is the best way to keep books?

To start keeping books, you will need some things. You will need a notebook, pencils and calculators, a printer, stapler, pen, stapler, envelopes and stamps, as well as a filing cabinet or drawer.

What does it entail to reconcile accounts?

A reconciliation is the comparison of two sets. The source set is called the “source,” while the reconciled set is called both.

The source includes actual figures. The reconciled shows the figure that should be used.

If someone owes $100 but you receive only $50, this would be reconciled by subtracting $50 from $100.

This ensures there are no errors in the accounting system.

What is the difference between accounting and bookkeeping?

Accounting refers to the study of financial transactions. Bookkeeping records these transactions.

These are two related activities, but separate.

Accounting deals primarily in numbers while bookkeeping deals with people.

Bookkeepers record financial information for purposes of reporting on the financial condition of an organization.

They ensure all books balance by correcting entries in accounts payable and accounts receivable.

Accountants examine financial statements in order to determine whether they conform with generally accepted accounting practices (GAAP).

If they are unsure, they might recommend changes in GAAP.

Bookskeepers record financial transactions in order to allow accountants to analyze it.

Statistics

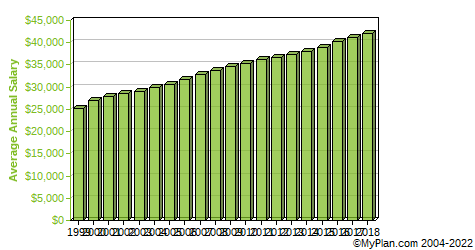

- The U.S. Bureau of Labor Statistics (BLS) projects an additional 96,000 positions for accountants and auditors between 2020 and 2030, representing job growth of 7%. (onlinemasters.ohio.edu)

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- According to the BLS, accounting and auditing professionals reported a 2020 median annual salary of $73,560, which is nearly double that of the national average earnings for all workers.1 (rasmussen.edu)

- In fact, a TD Bank survey polled over 500 U.S. small business owners discovered that bookkeeping is their most hated, with the next most hated task falling a whopping 24% behind. (kpmgspark.com)

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

External Links

How To

How to do bookkeeping

There are many types of accounting software available today. There are many types of accounting software available today. Some are free while others cost money. However, they all offer basic features like invoicing and billing, inventory management as well as payroll processing, point of sale systems and financial reporting. The following is a brief overview of the most widely used types of accounting software.

Free Accounting Software - This free software is often offered to personal use. It may have limited functionality (for example, you cannot create your own reports), but it is often very easy to learn how to use. You can also download data into spreadsheets with many free programs, which is useful if your goal is to analyze your company's financials.

Paid accounting software: Paid accounts can be used by businesses with multiple employees. They typically include powerful tools for managing employee records, tracking sales and expenses, generating reports, and automating processes. Most paid programs require at least one year's subscription fee, although there are several companies offering subscriptions that last less than six months.

Cloud Accounting Software. Cloud accounting software allows for remote access to your files using any mobile device such as smartphones and tablets. This program has been growing in popularity because it reduces clutter and saves space on your computer's hard drive. You don't even need to install any additional software. All you need to access cloud storage is an Internet connection.

Desktop Accounting Software: Desktop Accounting Software works on your computer, just like cloud accounting. Desktop software works in the same way as cloud software. It allows you to access files from any location, including via mobile devices. However, unlike cloud software, you must install the software on your computer before you can use it.

Mobile Accounting Software: Our mobile accounting software can be used on smartphones and tablets. These programs let you manage your finances while on the go. Although they offer less functionality than full-fledged desktop applications, they are still very useful for people who travel or run errands.

Online Accounting Software: This software is primarily designed for small businesses. It includes everything that a traditional desktop package does plus a few extra bells and whistles. Online software has one advantage: it doesn't require installation. Simply log on to the site and begin using the program. You'll also save money by not having to pay for local office costs.