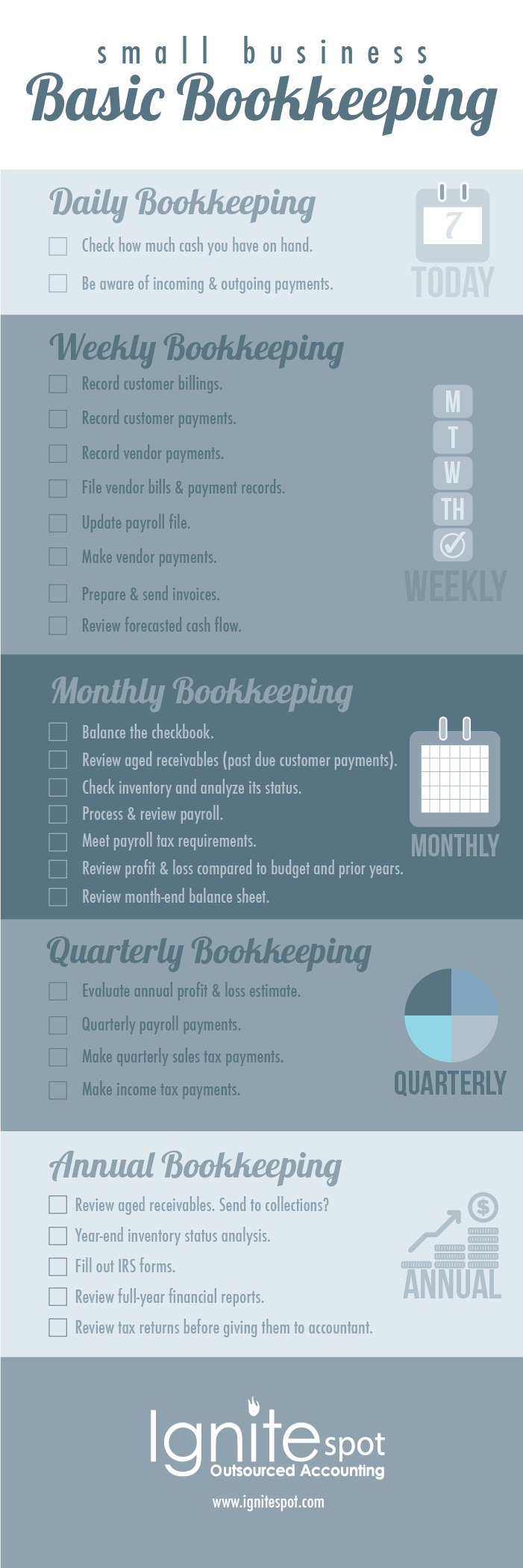

What does an accounts receivable record do for a business's financial health? These records track the money being exchanged between two businesses. These records allow businesses to track revenue, keep a steady cash flow and claim from third parties. Most businesses will allow a portion or all of their sales to be paid on credit. Credit is usually offered to customers who are regulars, clients with special needs, and all clients. A receivable is a situation in which a customer doesn't pay the amount owed.

Accounts receivable refers to a record that records the exchange between two companies.

Your business depends on accounts receivable to manage your cash flow management. These records help you understand where you stand in terms of the amount of money owed to you by clients. These records not only help you to stay calm in times of stress, but they also give you an accurate picture of how much money you owe. This information will allow you to make better business decisions and increase your cash flow.

A record of the amount of money owed by customers is called an accounts receivable. This amount is shown on your company's balance sheet. This is the amount due from a debtor within a specified year or time frame. You send out invoices, track payment, send reminders, then record the amount owed. After the customer has paid the balance, the account is considered an asset and revenue. Account payable is different from accounts receivable. It is dependent on the purchase or sale of goods and/or service.

It helps businesses recognize revenue when it is earned

Recognizing revenue is a key concept in accounting. When a company receives payment form a customer, revenue is earned. However, revenue recognition can be complex. Revenue in a retail setting is when a customer actually purchases a product and has paid for it. Revenue recognition is more complicated for a construction company. In order to sustain operations, businesses generally need enough revenue.

A business must know when a transaction occurred in order to accurately track its revenue. Recognizing revenue is critical to allow a company to track when a sale occurs or when a service is rendered. It is important that a customer's expectation is realistic so that it can be accounted for correctly. If the customer does not pay up-front, revenue recognition may not occur.

It helps businesses maintain a steady cash flow.

An efficient system for managing receivables is key to a healthy cash flow. Receivables include sales that a business expects to receive within a year. This is similar to the electric company charging customer for electricity after they've used it, but you haven't paid the money. These invoices can be recorded as current assets in your balance and general ledger.

An assessment of the cash flow statements can help you determine where improvements are needed. If you can't collect on all accounts, it may be possible to reduce the number of late-paying customer. You can use slower periods to put in more efficient systems if you are still manually processing invoices. It's easy to overlook potential rough patches and not realize they've crept up on your company. A steady cash flow can prevent stress and uncertainty in your business.

It assists businesses in collecting claims from third-parties

Businesses can use accounts receivables to help them collect third-party claims for goods and services. These accounts are collected from customers as well as third parties who have made payment arrangements. This is an important aspect of any business. Even if a customer is not paying immediately, you can follow up with a phone call or email. You should not follow-up with good paying customers. This could upset them and make them feel hounded. Follow-up should only be done if the customer has not paid you. Be prepared to do so.

An accurate picture of the company's financial situation can be used to help track cash flow and account receivable helps companies monitor their cash flow. It can also help the business to understand how much money it owes customers. Bad decisions can be made if accounts receivables don't get properly maintained. You can get a better picture of your company's financial health if you follow proper accounting and invoicing practices.

FAQ

What is an accountant and why are they so important?

An accountant keeps track of all the money you earn and spend. An accountant also records how much tax you have to pay and the deductions that are allowed.

An accountant can help you manage your finances and keep track of your incomes and expenses.

They are responsible for preparing financial reports that can be used by individuals or businesses.

Accounting professionals are required because they need to be able to understand all aspects of the numbers.

Additionally, accountants assist with tax filing and make sure that taxpayers pay the least amount of tax.

What are the steps to get started with keeping books?

You will need a few things to begin keeping books. A notebook, pencils or a calculator are all you will need to start keeping books.

What does an auditor do?

An auditor looks for inconsistencies between the information given in the financial statements and the actual events.

He checks the accuracy of the figures provided by the company.

He also confirms the accuracy of the financial statements.

Accounting: Why is it useful for small-business owners?

The most important thing you need to know about accounting is that it's not just for big businesses. It's also useful for small business owners because it helps them keep track of all the money they make and spend.

If you run a small business, you likely know how much money comes in each month. But what if your accountant doesn't do this for a monthly basis? You might be wondering about your spending habits. You could also forget to pay bills on-time, which could impact your credit score.

Accounting software makes it simple to track your finances. There are many choices. Some are free while others cost hundreds to thousands of dollars.

You will need to learn the basic functions of every accounting system. It will save you time and help you understand how to use it.

These three tasks are essential.

-

Record transactions in the accounting system.

-

Keep track of your income and expenses.

-

Prepare reports.

Once you've mastered these three things, you're ready to start using your new accounting system.

Statistics

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- The U.S. Bureau of Labor Statistics (BLS) projects an additional 96,000 positions for accountants and auditors between 2020 and 2030, representing job growth of 7%. (onlinemasters.ohio.edu)

- Given that over 40% of people in this career field have earned a bachelor's degree, we're listing a bachelor's degree in accounting as step one so you can be competitive in the job market. (yourfreecareertest.com)

- BooksTime makes sure your numbers are 100% accurate (bookstime.com)

- According to the BLS, accounting and auditing professionals reported a 2020 median annual salary of $73,560, which is nearly double that of the national average earnings for all workers.1 (rasmussen.edu)

External Links

How To

Accounting for Small Business

Accounting is a critical part of running a small business. This involves tracking income and expenses as well as preparing financial reports and tax payments. You may also need to use software programs like Quickbooks Online. There are many different ways you can do your small business accounting. You must choose the right method for you, based on your requirements. Below we have listed some of the top methods for you to consider.

-

You can use paper accounting. Paper accounting is a good option if you prefer simplicity. This method is simple. You just need to keep track of your transactions each day. However, if you want to make sure that your records are complete and accurate, then you might want to invest in an accounting program like QuickBooks Online.

-

Use online accounting. Using online accounting means that you can easily access your accounts at any time and anywhere. Wave Systems, Freshbooks and Xero are all popular choices. These software programs allow you to manage finances, pay bills, generate reports, send invoices, and more. They offer great features and benefits, and they are easy to use. These programs are great for saving time and money in accounting.

-

Use cloud accounting. Cloud accounting is another option. It allows you to store your data securely on a remote server. Cloud accounting is a better option than traditional accounting systems. It doesn't require you to purchase expensive hardware or software. Second, it offers better security because all your information is stored remotely. It takes the worry out of backups. Fourth, it makes it easier for you to share your files with other people.

-

Use bookkeeping software. Bookkeeping software is similar with cloud accounting. However you must purchase a computer in order to install the software. After installing the software, you will be able to connect to the internet so that you can access your accounts whenever you want. You can also view your balances and accounts right from your computer.

-

Use spreadsheets. Spreadsheets enable you to manually enter your financial transactions. One example is a spreadsheet you can use to track your daily sales. A spreadsheet's advantage is that you can make changes to them at any time without having to change the whole document.

-

Use a cash book. A cashbook is a ledger where you write down every transaction that you perform. There are many different shapes and sizes of cashbooks depending on how much room you have. You have the option of using a different notebook for each month, or a single notebook that covers several months.

-

Use a check register. A check register is a tool that helps you organize receipts and payments. Once you have scanned the items, you can transfer them into your check register. You can then add notes to help remember what you bought later.

-

Use a journal. Journals are a logbook that helps you keep track of your expenses. This is best for those who have recurring expenses like rent, insurance, and utilities.

-

Use a diary. Use a diary. It is simply a notebook that you keep for yourself. It can be used to track your spending habits and plan your finances.