You may be curious about the job of a virtual bookkeeper if you're looking to hire one. This article will explain the benefits of virtual bookkeeping, the costs involved, and how to get started. This article is designed to help you find the perfect candidate. Once you have completed the questionnaire, you can start working as a virtual accountant immediately. And, in the meantime, get a feel for the job by reading on!

Virtual bookkeeper job duties

Your services can be promoted in many ways, including as a virtual accountant. A good way to get the word out is to advertise in bookkeeping communities. Ask people you know for recommendations and use social selling as a marketing tool. It is important to keep your website updated and to offer value to your clients. Your branding will help you attract more clients. If you are not sure how to do this, here are some ways to promote yourself:

The best thing about virtual bookkeeping is the low cost. Virtual bookkeeping offers a cost-effective alternative to hiring a fulltime accountant. A virtual bookkeeper will give you an objective view of your business' financial health which is essential for sound decisions.

Cost of hiring virtual bookkeeper

Apart from the above benefits, hiring a virtual bookkeeper could save you money on payroll taxes as well as overhead. California employers are responsible in California for Social Security, Medicare taxes and Employment Training Tax. California Tax has more information. A virtual bookkeeper can be hired for as low as $50 per month, or as high as $3,000 per monthly depending on the volume.

A virtual bookkeeper is able to work remotely from anywhere in this world. This makes it much more affordable that hiring a local person to handle your bookkeeping needs. Another benefit of using a virtual bookkeeper to manage your accounting needs is the lower cost. As their costs are divided among multiple clients, you only pay for what they do. Hourly rates and fixed fees can be paid for virtual bookkeepers.

Learn online to become a virtual bookkeeper

Online bookkeeping courses are a good way to get started in the virtual world of bookkeeping. Many of these courses include quizzes and step-by–step lessons that can help you understand the business. Some courses give you access online to a network of experienced bookkeeping professionals who can help you gain clients and gain experience. It is a good idea to enroll in an online course if you want to become a virtual bookkeeper.

Learning the skills and techniques necessary to be a virtual bookkeeper is the first step. Once you have mastered your skill set, you can start earning $60 an hour or more by working for private clients. You can also watch videos in your online course to get more information about the business. Kirsty was previously a full-time Business Manager before she decided she wanted to become a virtual Bookkeeper. Now she has 11 clients and generates more than $3,000 per monthly.

Virtual bookkeepers can use freelancing platforms

You can upload your resume and get matched up with clients through freelancing platforms for virtual bookskeepers. These platforms are full of tools and resources that can help you find work. These are some of our favorite platforms for remote job opportunities as bookkeepers. These platforms can help you make more money while also giving you a part-time position.

Most freelancers charge an hourly rate. The more transactions that you have per month, the more you will pay. You should be prepared to disclose your hourly rate and other details, such as your experience and skills and the number transactions per month, when looking for a virtual Bookkeeper. Some freelancers only work with cash basis accounting, while others work with accrual basis. You can hire a virtual accounting service to help you decide which accounting system works best for your business.

FAQ

How do I start keeping books?

For you to begin keeping your books, you'll need a few things. A notebook, pencils or a calculator are all you will need to start keeping books.

What is a Certified Public Accountant (CPA)?

A certified public accountant (C.P.A.) is a person with specialized knowledge in accounting. He/she knows how to prepare tax returns and assist businesses in making sound business decisions.

He/She monitors cash flow for the company and makes sure the company runs smoothly.

What happens if I don't reconcile my bank statement?

If you fail to reconcile your bank statement, you may not realize that you've made a mistake until after the end of the month.

At this point, you will need repeat the entire process.

What type of training is required to become a Bookkeeper?

Basic math skills are necessary for bookkeepers. They need to be able to add, subtract, multiply, divide, fractions and percentages.

They must also be able to use a computer.

Many bookkeepers have a highschool diploma. Some may even hold a college degree.

What are the signs that my company needs an accountant?

Many companies hire accountants when they reach certain size levels. A company might need an accountant when it makes $10 million annually or more in sales.

However, there are some companies that hire accountants regardless if they have a small business. These include small companies, sole proprietorships as well partnerships and corporations.

A company's size doesn't matter. Accounting systems are the only thing that matters.

If it does then the company requires an accountant. And it won't.

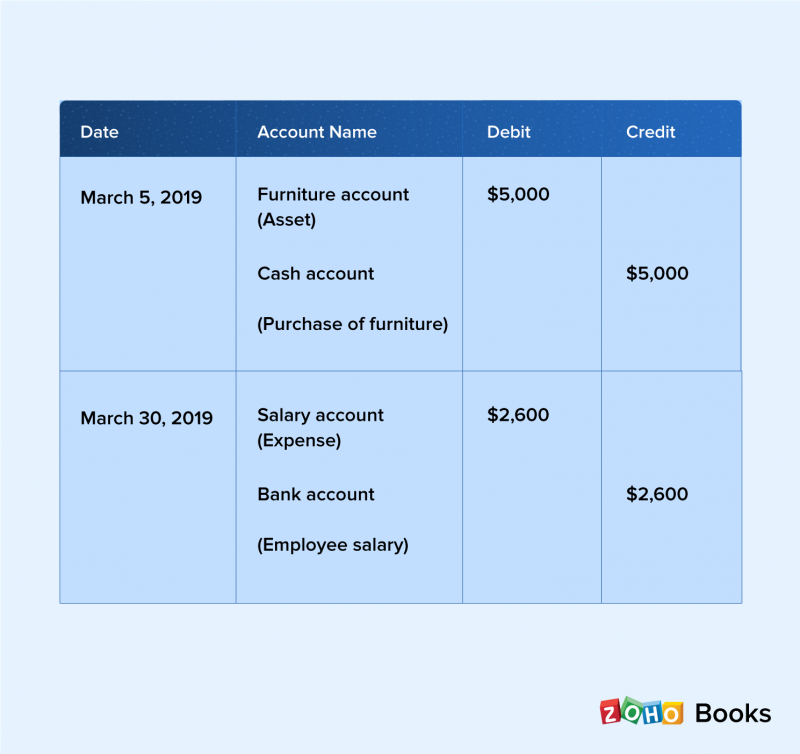

What is bookkeeping exactly?

Bookkeeping is the art of keeping records of financial transactions for individuals, businesses, and organizations. This includes all income and expenses related to business.

Bookkeepers maintain financial records such as receipts. They prepare tax returns, as well as other reports.

What is the difference between bookkeeping and accounting?

Accounting is the study of financial transactions. Bookkeeping records these transactions.

They are both related, but different activities.

Accounting deals primarily with numbers, while bookkeeping deals primarily with people.

For reporting purposes on an organization's financial condition, bookkeepers keep financial records.

They adjust entries in accounts payable, receivable, and payroll to ensure that all books are balanced.

Accounting professionals examine financial statements to determine if they are in compliance with generally accepted accounting principles.

They may suggest changes to GAAP if they do not agree.

Bookskeepers record financial transactions in order to allow accountants to analyze it.

Statistics

- In fact, a TD Bank survey polled over 500 U.S. small business owners discovered that bookkeeping is their most hated, with the next most hated task falling a whopping 24% behind. (kpmgspark.com)

- According to the BLS, accounting and auditing professionals reported a 2020 median annual salary of $73,560, which is nearly double that of the national average earnings for all workers.1 (rasmussen.edu)

- a little over 40% of accountants have earned a bachelor's degree. (yourfreecareertest.com)

- BooksTime makes sure your numbers are 100% accurate (bookstime.com)

- The U.S. Bureau of Labor Statistics (BLS) projects an additional 96,000 positions for accountants and auditors between 2020 and 2030, representing job growth of 7%. (onlinemasters.ohio.edu)

External Links

How To

How to Become a Accountant

Accountancy is the science of recording transactions and analyzing financial data. Accounting can also include the preparation of reports or statements for various purposes.

A Certified Public Accountant is someone who has passed and been licensed by the state board.

An Accredited Finance Analyst (AFA), an individual who meets certain requirements established by the American Association of Individual Investors. A minimum of five year's investment experience is required before an individual can be made an AFA. To pass the examinations, they must have a good understanding of accounting principles.

A Chartered Professional Accountant is also known by the name chartered accountant. This is a professional accountant who received a degree at a recognized university. CPAs must comply with the Institute of Chartered Accountants of England & Wales’ (ICAEW) educational standards.

A Certified Management Accountant (CMA) is a certified professional accountant specializing in management accounting. CMAs need to pass exams administered through the ICAEW, and must continue education requirements throughout their careers.

A Certified General Accountant (CGA) member of the American Institute of Certified Public Accountants (AICPA). CGAs are required to take several tests; one of these tests is known as the Uniform Certification Examination (UCE).

International Society of Cost Estimators, (ISCES), offers the Certified Information Systems Auditor (CIA), a certification. Candidates for the CIA certification must complete three levels, which include coursework, practical training and a final assessment.

Accredited Corporate Compliance officer (ACCO) is a distinction granted by the ACCO Foundation, and the International Organization of Securities Commissions. ACOs must possess a Bachelor's Degree in Finance, Business Administration, Economics, or Public Policy. They must pass two written exams, and one oral exam.

The National Association of State Boards of Accountancy offers the certification of Certified Fraud Examiners (CFE). Candidates must pass 3 exams and score a minimum of 70 percent.

International Federation of Accountants is accredited a Certified Internal Audior (CIA). The International Federation of Accountants (IFAC) requires that candidates pass four exams. These include topics such as auditing and risk assessment, fraud prevention or ethics, as well as compliance.

An Associate in Forensic Accounting (AFE) is a designation given by the American Academy of Forensic Sciences (AAFS). AFEs must have graduated with a bachelor’s degree from an approved college or university in any other study area than accounting.

What does an auditor do? Auditors are professionals who conduct audits of organizations' internal controls over financial reporting. Audits can either be done randomly or based on complaints about financial statements received by regulators.